Div 296 will tax unrealised gains and more

Taxation of unrealised capital gains has been contentiously debated among OECD countries. Australia appears set to join the ranks of Norway and Switzerland, with the Labor government seeking to pass legislation that effectively taxes unrealised capital gains.

This will be a major step in tax law in Australia and may result in other gains outside of the superannuation environment being subject to an unrealised tax in future years if the government is successful in taxing unrealised gains in superannuation funds.

Overview

The Treasury Laws Amendment (Better Targeted Superannuation Concessions) Bill 2023 (bill) proposes to insert new Division 296 (Div 296) into the Income Tax Assessment Act 1997 (Cth) (ITAA) to impose an extra 15 per cent on certain member’s superannuation balances.

Broadly, from 1 July 2025, the Div 296 tax will apply where a member’s total superannuation balance (TSB) exceeds $3 million and there has been an increase in their TSB at the end of the relevant income year (as adjusted for a wide range of withdrawals and contributions) compared to their TSB just before the start of that income year. This movement in the adjusted TSB is termed ‘superannuation earnings’.

The proportion of the superannuation earnings that corresponds with the percentage of an individual’s TSB that exceeds $3 million makes up the ‘taxable superannuation earnings’ (TSE). The TSE will be assessed to the individual and subject to tax at the rate of 15 per cent.

The bill also proposes to make a number of exceptions and numerous other consequential and miscellaneous amendments to the ITAA, Taxation Administration Act 1953 (Cth), and other Commonwealth laws to give effect to this measure.

There is considerable complexity to the new tax, and this article provides a simplified analysis of several key aspects of Div 296 that is due to commence on 1 July 2025 for the 2025-26 and subsequent income years.

How this bill will work

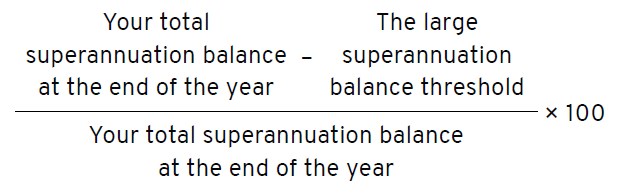

An individual has TSE for an income year if their TSB at the end of that year is greater than $3 million and the amount of their superannuation earnings for the year is greater than nil. (Note that the Greens are seeking to reduce this threshold to $2 million).

The total amount of TSE for an income year is worked out by first determining the percentage of the TSB at the end of the year that exceeds the threshold according to the following formula:

The percentage provided by the formula is then multiplied by the amount of superannuation earnings for the year to provide the amount of TSE. This is achieved by applying the following formula:

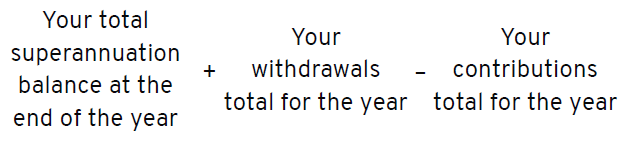

The amount of an individual’s basic superannuation earnings for an income year is determined by subtracting their previous TSB (their TSB immediately before the start of the income year) from their current adjusted TSB (their adjusted TSB at the end of that year), as follows:

The adjusted TSB reflects a modified closing superannuation balance after considering the effect of a range of withdrawals and contributions that would otherwise overstate or understate earnings. This area is complex, given the nature and number of withdrawals and contributions that may result in an adjusted TSB. As noted above, this is a simplified explanation of a very complex tax.

The draft bill will result in a member being liable to pay tax on TSE under proposed s 296-15 of the ITAA. A 15 per cent tax rate will then be applied to that member’s Div 296 earnings, and a separate assessment to the member will be issued; the Div 296 assessment will be in addition to any income tax or Div 293 tax assessment.

Example on how Div 296 will apply to Sarah

For example, Sarah’s TSB on 30 June 2026 is $6 million. The proportion of her TSB that exceeds $3 million is 50 per cent ([$6 million – $3 million] ÷ $6 million). In this case, 50 per cent of her TSE will attract the additional tax. A flat tax rate of 15 per cent is then applied to the proportion of earnings attributable to an individual’s balance over $3 million.

For example, Sarah’s calculated earnings are $650,000; however, only 50 per cent of these earnings are attributed to her TSB that exceeds $3 million and attract the additional 15 per cent tax.

Sarah’s tax liability is $48,750 (15 per cent × $650,000 × 50 per cent). This tax in addition to her other income tax, Div 293 and any tax payable on Sarah’s superannuation balance by the trustee of the fund.

Members can elect to obtain a release authority

Members will have 84 days from the issue of an assessment to pay their Div 296 tax liability. However, a member will be given the opportunity to withdraw money from their superannuation fund to pay Div 296 tax under a ‘release authority’ arrangement that is similar to what is in place for Div 293 tax. Members will have 60 days to elect to release a certain amount from one or more of their superannuation funds to pay their Div 296 tax without needing to satisfy the usual conditions of release, such as retirement after attaining 60.

Div 296 implications

While broadly supportive of the principle that tax concessions for superannuation should be subject to certain limits, numerous professional bodies have serious concerns with the following aspects of the new measures:

· The imposition of a tax on unrealised gains: especially as the new tax will adversely impact those with illiquid assets, such as real estate, especially farmers, and who may have no readily available funds to pay the tax. Also, there have been concerns raised that Div 296 will, to some extent, give rise to a tax on a tax given the member pays tax on unrealised gains and the fund pays tax on realised gains. Numerous professional bodies have submitted that SMSF members should be taxed on actual taxable income or a deemed annual earnings rate rather than being taxed on unrealised gains.

· Negative superannuation earnings are quarantined: they can only be used to offset future earnings and do not give rise to a refund. If unrealised gains are to be subject to tax, tax symmetry and fairness suggests that a refund should be provided for any negative superannuation earnings.

· The $3 million threshold is not indexed: while the new measure is initially expected to impact around 80,000 members in the 2025-26 income year, with increasing investment values and contributions to superannuation over time, as well as inflationary pressure, over time, many more members will be captured by this threshold.

· A member will have no ability to withdraw their superannuation balance when it exceeds $3 million and they have not yet satisfied a condition of release, e.g., a member who is 50 and has had significant growth in their superannuation assets has no option but to pay the new tax. This is a major change in superannuation policy, and submissions have been made that members should be entitled to withdraw any excess above the threshold to avoid the tax.

Prior to the 3 May 2025 federal election, the bill was stalled in the Senate largely due to concerns about taxing unrealised gains and the lack of indexation. Numerous professional and industry bodies are expected to continue to advocate for changes to address their concerns. However, the reconstituted government in both houses of Parliament in favour of the current government will make any changes more difficult to achieve.

Report from the University of Adelaide

After reviewing data on more than 720,000 SMSF members each year over the financial years ending in 2021 and 2022, the University of Adelaide’s International Centre for Financial Services report concluded that:

“Taxation on unrealised capital gains is rare among OECD countries, and rarer still in OECD pension systems. Australia’s tax system clearly delineates between income and capital gain taxes (CGT), and the CGT regime, which has been in place now for almost 40 years, is based primarily on realised gains evidenced by completed transactions. Given both the benchmarking to other OECD nations and Australia’s own economic history, we interpret the structure of the current proposal – to reduce superannuation tax concessions for individuals with TSBs in excess of $3 million – as a somewhat radical departure from existing taxation policy, with potentially far broader consequences than just those outlined by Treasury in their consultation paper.

Deferring the taxation of unrealised gains until they are realised is very likely to ‘grow the pie’ for both superannuants, and for those taxing superannuants, in the longer term.

Selling illiquid assets is typically associated with substantial transaction costs, and the government’s proposal to cover the new liability with funds external to superannuation is unlikely to be possible for all affected members.

We estimate an approximate 4-fold increase in the rate of liquidity problems, from 3.1 per cent to 13.5 per cent, once we account for members meeting the added tax expense in a prior period. This implies an additional cumulative liquidity risk factor for affected members.

There might be as many as 49,000-50,000 SMSF members in Australia that will be impacted by the changes in tax concessions for super, year-on-year, based on our balanced panel.”

Is a 1 July 2025 start date achievable?

The bill proposes to commence the first taxable period on 1 July 2025. However, the bill still needs to be finalised as law prior to systems being implemented to administer the new tax, including collecting a massive amount of data from most superannuation funds so the ATO can start issuing Div 296 assessments from 1 July 2026.

This naturally requires considerable work and investment in software, and system changes are needed to implement the new Div 296 tax. Even if the legislation is passed soon, the commencement date of 1 July 2025 appears ambitious and could prove difficult for many digital service providers and possibly even the ATO. Moreover, every impacted superannuation fund will need to change its systems and communicate to members the outline of this new and complex tax.

Members of large and small funds should be provided adequate notice to plan ahead, especially where to obtain the money to pay for this additional tax, especially if they are being taxed on unrealised gains.

Conclusions

The relatively short time frame the government has to pass this legislation and for industry and advisers to update systems to implement the new tax for a 1 July 2025 commencement seems optimistic.

While the ATO performs the calculations and issues the assessments from its systems and data, advisers will need to understand how the systems and processes work so they can assist their clients on Div 296 matters. Undoubtedly, there will be errors, issues and teething problems in implementing and refining the systems that relate to this new tax.

This article is for general information only and should not be relied upon without first seeking advice from an appropriately qualified professional. The above does not constitute financial product advice. Financial product advice can only be obtained from a licenced financial adviser under the Corporations Act 2001 (Cth).

Subscribe to the

BULLETIN

Get the latest news and opinions delivered to your inbox each morning

Subscribe