Triggering your bring forward NCC cap post 1 July 2017

The eligibility criteria for individuals who wish to bring forward their non-concessional contributions cap post 1 July 2017 is more rigorous and complex than ever before.

However, bringing forward an individual’s NCCs cap will still remain a popular strategy to boost an individual’s superannuation balance. Special transitional arrangements apply where an individual triggered but did not fully use up a bring forward of their NCCs cap prior to 1 July 2017.

These transitional arrangements are not discussed in this article. Instead, this article examines the criteria that individuals must meet before they can trigger a ‘bring forward’ of their NCCs cap post 1 July 2017, and highlights some of the complexities associated with utilising this strategy post 1 July 2017.

Eligibility criteria for an individual who wishes to bring forward their NCCs cap

An individual’s NCCs cap for a financial year is four times their concessional contributions (CCs) cap for the year. For the 2017-18 financial year (FY2018), the CCs cap is $25,000, and this amount will be subject to indexation in later FYs. Accordingly, for FY2018, the NCCs cap is $100,000.

In order for an individual to trigger a ‘bring forward’ of their NCCs cap post 1 July 2017, they must satisfy the eligibility criteria in s 292-85(3) of the Income Tax Assessment Act 1997 (Cth) (ITAA 1997). These criteria are broadly summarised as follows:

- The individual’s NCCs for the first year must exceed the general NCCs cap for that year. For example, the individual’s NCCs for FY2018 must exceed $100,000;

- Immediately before the start of the first year, the individual’s total superannuation balance (TSB) does not equal nor exceed the general transfer balance cap (TBC) for the first year. For FY2018, the general TBC is $1,600,000, and this amount will be subject to indexation in later FYs;

- The individual is under 65 years at any time in the first year;

- The individual’s NCCs cap for the first year does not constitute a second year or third year of a ‘bring forward’ of the individual’s NCCs cap that was previously triggered; and

- The difference (also known as the first year cap space) between the general TBC for the first year and the individual’s TSB immediately before the start of the first year exceeds the general NCCs cap for the first year. For example, assuming FY2018 is the first year, the difference between $1,600,000 and the individual’s TSB immediately before the start of FY2018 must exceed $100,000 in order for the individual to be eligible to trigger a ‘bring forward’ of their NCCs.

Calculating an individual’s NCCs cap for each year

Once an individual satisfies the eligibility criteria and decides to trigger a ‘bring forward’ of their NCCs cap post 1 July 2017, they will need to calculate their NCCs cap in each relevant year of the ‘bring forward’ period. The below broadly summarises the rules for each year of the ‘bring forward’ period.

First year of bring forward

- If the first year cap space does not does not exceed an amount equal to twice the general NCCs cap for the first year, the individual’s NCCs cap for the first year is twice the general NCCs cap; and

- If the first year cap space exceeds an amount equal to twice the general NCCs cap for the first year, the individual’s NCCs cap for the first year is three times the general NCCs cap.

Second year of bring forward

- If the individual’s TSB immediately before the start of the second year is less than the general TBC for the second year, and their NCCs for the first year fell short of their cap for the first year, their NCCs cap for the second year is the amount of the shortfall; and

- Otherwise, the individual’s NCCs cap for the second year is nil.

Third year of bring forward

- If the individual’s TSB immediately before the start of the third year is less than the general TBC for the third year, and their NCCs for the second year fell short of their cap for the second year, their NCCs cap for the third year is the amount of the shortfall;

- If the individual’s TSB immediately before the start of the third year is less than the general TBC for the third year, their cap for the second year is nil, and their NCCs for the first year fell short of their cap for the first year, their NCCs cap for the third year is the amount of the shortfall; and

- Otherwise, the individual’s NCCs cap for the third year is nil.

As noted above, the rules regarding the third year of bring forward do not apply if the first year cap space does not exceed an amount equal to twice the general NCCs cap for the first year. This effectively means that the ‘bring forward’ period can be either two years or three years depending on the amount of the first year cap space.

‘Bring forward’ period of two years versus three years

We illustrate the differences between calculating an individual’s ‘bring forward’ NCCs cap under a three-year ‘bring forward’ period and under a two-year ‘bring forward period by contrasting two examples below.

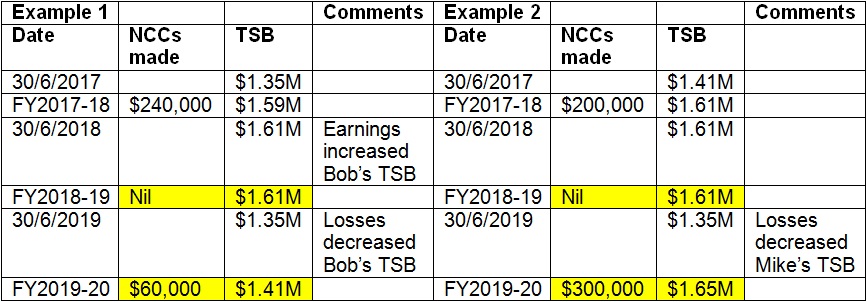

Example 1

Consider the example of Bob. (This example assumes that the general TBC remains at $1,600,000 and the general NCCs cap remains at $100,000 in all relevant years.)

Bob’s TSB is $1,350,000 as at 30 June 2017. On 1 August 2017, Bob is 60 years old and the difference between the general TBC and his TSB is $250,000. Accordingly, if Bob decides to trigger his NCCs cap, his NCCs cap for the first year is $300,000 (e.g. three times the general NCCs cap). On 1 August 2017, Bob triggers his bring forward NCCs cap by making an NCC of $240,000. In making this NCC, Bob has used up $240,000 of the $300,000 NCCs cap available to him. This brings his TSB to $1,590,000. Bob does not make any further NCCs during FY2018. However, earnings increase Bob’s TSB to $1,610,000 as at 30 June 2018.

As Bob’s TSB before the start of FY2019 is greater than the general TBC of $1,600,000, his NCCs cap for the second year is nil and he cannot make an NCC during the entire FY2019. However, losses decrease Bob’s TSB to $1,350,000 as at 30 June 2019.

Bob’s TSB before the start of FY2020 is less than the general TBC of $1,600,000, his NCCs cap for the second year is nil, and the NCC that he made in the first year falls short of his cap for the first year by $60,000 ($300,000 - $240,000). Accordingly, Bob makes an NCC of $60,000 during FY2020, which brings his TSB to $1,410,000 as at 30 June 2020.

Example 2

Consider the example of Mike. (This example assumes that the general TBC remains at $1,600,000 and the general NCCs cap remains at $100,000 in all relevant years.)

Mike’s TSB is $1,410,000 as at 30 June 2017. On 1 August 2017, Mike is 60 years old and the difference between the general TBC and his TSB is $190,000. Accordingly, if Mike decides to trigger his NCCs cap, his NCCs cap for the first year is $200,000 (e.g. two times the general NCCs cap). On 1 August 2017, Mike triggers his bring forward NCCs cap by making an NCC of $200,000. In making this NCC, Mike has used up the entire NCCs cap available to him. This brings his TSB to $1,610,000. Mike cannot and does not make any further NCCs during FY2018. Mike’s TSB is $1,610,000 as at 30 June 2018.

As Mike’s TSB before the start of FY2019 is greater than the general TBC of $1,600,000, his NCCs cap for the second year is nil he cannot make an NCC during the entire FY2019. Even if his TSB was less than the general TBC of $1,600,000, he has used up his NCCs cap for the first year, his NCCs cap for the second year is nil and he cannot make an NCC during the entire FY2019. However, losses decrease Mike’s TSB to $1,350,000 as at 30 June 2019.

Mike’s TSB before the start of FY2020 is less than the general TBC of $1,600,000, what is his NCCs cap for the third year — is it $100,000 or another amount?

The answer is: Mike’s NCCs cap for FY2020 is four times his CCs cap, e.g. $100,000, unless this third year becomes a new first year under another trigger of the bring forward NCCs cap. As the difference between the general TBC and Mike’s TSB is $250,000, if Mike decides to trigger another bring forward, his NCCs cap for the new first year is $300,000 (e.g. three times the general NCCs cap). Accordingly, Mike makes an NCC of $300,000 during FY2020, which brings his TSB to $1,650,000 as at 30 June 2020.

We summarise the relevant figures of Example 1 and Example 2 in the table below.

The main point to take away from these examples are that if an individual is considering triggering a ‘bring forward’ of their NCCs cap, careful planning and monitoring of their TSB is needed. It is interesting to note from the above examples that immediately prior to the first year (i.e. on 30 June 2017), Bob and Mike’s TSB only differed by $6,000. Also, as at the end of the second year (i.e. 30 June 2019), Bob and Mike’s TSB were both the same, being $1,350,000. However, because of the difference in their first year cap space, Mike was effectively subject to a two-year ‘bring forward’ period, and could trigger another ‘bring forward’ of his NCCs cap immediately after the end of the two-year period.

- An individual’s TSB immediately before the start of the first year determines whether they will be subject to a ‘bring forward’ period of two years or three years. Where an individual is contemplating triggering a ‘bring forward’ of their NCCs cap while still within a few years of attaining age 65 years, the duration of the ‘bring forward’ period could determine whether they can have another chance at triggering a ‘bring forward’ just prior to attaining age 65 years.

- An individual’s TSB will also be relevant in determining whether an individual can make an NCC in the second year or third year of the relevant ‘bring forward’ period.

Conclusion

The law in relation to ‘bring forward’ of an individual’s NCCs cap is a complex area of law and where in doubt, expert advice should be obtained. Naturally, for advisers, the Australian Financial Services Licence under the Corporations Act 2001 (Cth) and tax advice obligations under the Tax Agent Services Act 2009 (Cth) need to be appropriately managed to ensure advice is legally provided.

Joseph Cheung, lawyer and Daniel Butler, director, DBA Lawyers

Subscribe to the

BULLETIN

Get the latest news and opinions delivered to your inbox each morning

Subscribe