The short-term focus of too many investors is extremely destructive of the wealth they have built up over their lifetimes. The sharp market sell-offs since mid-2015 demonstrate periods where primal fear takes over and many people sell purely because others are selling. At the individual level, ‘short-termism’ can slash the value of their capital and limit a their ability to fund a comfortable retirement. It is also damaging at society level as an acute emphasis on near-term performance incentivises corporates to pursue quick-fix remedies to prop up profits, resulting in sub-optimal, longer-term outcomes.

SMSF practitioners can help their clients generate better results by ensuring their client’s investment choices are about long-term trends, particularly when they choose businesses that are competitively well placed to flourish. As sentiment is the key driver of short-term share prices, investors with a long-term view can use market selloffs as opportunities to buy attractive companies more cheaply. These investors benefit as share prices rise over time to their underlying true worth, without necessarily knowing exactly when this will occur.

There are five key long-term investment themes that can be identified for the next decade. Well-positioned companies benefiting from these trends should be on the shortlist for long-term client portfolios.

Technological disruption

Innovation is dramatically altering a great number of industries at speeds rarely seen before. Investment opportunities are available in the disruptors themselves as well as companies that benefit from the new technologies.

• In financial services, business managers are reappraising their approaches as digitisation reduces the cost to service customers across banking, wealth management and insurance. For instance, there appears to be tremendous potential for developing blockchain technology to remove multiple post-financial transaction back-office layers from banks and broking firms. A blockchain is a public ledger of all transactions.

• In energy, new technologies have allowed rapid expansion in supply from shale and other unconventional natural gas resources, while new batteries are being developed to enable large-scale energy storage.

• Healthcare is being revolutionised via mobile health, wearable sensors and next-generation genomics, which assists medical practitioners to manipulate genes and improve health diagnostics and treatments.

• In education, online resources are reducing costs and lifting teaching standards no matter where the student is.

The shift from traditional media and retail to online/digital has been occurring for a number of years. Take-up of online television and movie services like Netflix and music services like Spotify and Pandora demonstrate how rapidly consumers can switch to new digital subscription content offers from live-to-air networks. Many traditional retailers are yet to embrace digital technology as a strategic focus, being held back by legacy systems and old business practices. This leaves them prone to attack from younger and more flexible and scalable rivals.

Disruptive technologies are in strong demand due to the better consumer experiences that are being offered. Innovative solutions are fulfilling customer needs in far more compelling ways. New consumer products and services are making consumers’ lives easier and new business solutions are helping companies expand revenues and reduce costs. Social media platforms, for example, allow companies to cut marketing costs as well as reach new audiences. Websites like LinkedIn, Twitter and Google+ are among the cheapest arenas in history for companies to distribute their marketing content.

Disruptive forces should continue for some time due to rapid declines in start-up costs, especially as digitisation spreads, computer power increases and digital device use surges. New entrants can quickly challenge traditional provider profits as they are devoid of the encumbrances of inherited cost bases and old-fashioned cultural approaches.

The ‘Internet of things’ – the ability to transfer data over a network without human interaction – is another game-changing area of advancement. Business consultancy McKinsey & Company believes that global value of US$4 trillion to US$11 trillion will be created by 2025 as this technology becomes more prevalent. Some of the areas set to benefit most are factories, through more efficient operations management and predictive maintenance, public infrastructure, through better traffic control and resource management, healthcare, though better monitoring and management of illness, and retail, through self-checkout and smarter customer relationship management.

New technologies are creating powerful ‘network effect’ opportunities. Network effects relate to goods and services that become more valuable with increasing numbers of users. New telephone networks are a good example – if only one person uses a new network, they will not be able to call anyone else! As more people join the network it becomes increasingly useful.

New marketplace providers offer better user experiences with more connectivity and value-added technology features, like the property data and map information offered on realestate.com.au.

Facebook’s value proposition is connecting people with their friends. Its utility is different according to each user’s situation and time budget. The ability to capture user content extends the service. As more users comment on websites like TripAdvisor, online recommendations and endorsements become more helpful.

Emerging Asian middle class

Continued explosive growth of China and India’s middle classes create opportunities for consumer goods suppliers with offerings diversified beyond the standardised products commonly sold in these regions. Entertainment, food service, technology and other industries stand to benefit.

As emerging market wealth increases, there is rapid growth in the number and the purchasing power of the middle-class population. Most of the new members of the middle class are from China and India. The World Bank expects the global middle class to more than double from 430 million to 1.2 billion people between 2000 and 2030, with most of this growth from emerging markets.

Consumption growth in China remains strong despite the recent slowing in overall growth. Consumption as a percentage of Chinese GDP declined from 51 per cent in 1985 to 34 per cent in 2013 as a result of efforts to boost growth through investment, according to McKinsey. As a part of its ‘rebalancing’, just returning consumer spending back to 2005 levels of 43 per cent would create the largest consumer market in the world.

As for India, McKinsey estimates that if current high growth continues, it will rise from being the world’s twelfth-largest consumer market to the fifth by 2025. In this period, more than 291 million people will move out of abject poverty, and the middle class will expand more than 10 times to 583 million people. During that period, India’s middle class will rise to 41 per cent of the overall population from five per cent now. The wealthiest Indians will number more than 23 million.

As wealth increases, the proportion of income spent on discretionary items rises. Luxury brand producers are clear beneficiaries via the greater ability to purchase status symbols and rewards for hard work. Demand for services is also likely to rise, particularly in education, financial services and local and international travel and leisure. Demand for western-style food is also likely to grow.

Ageing western world populations

Ageing baby boomers and extended life expectancy is increasing the proportion of the population in older-age categories, boosting demand for services like healthcare and financial services. Ageing and longevity leads to greater spending on medicines and treatments as well as services like leisure, aged care, insurance and wealth management.

The proportion of developed country populations aged 60 or more grew to 23 per cent in 2013 from 12 per cent in 1950, according to the World Bank. This figure is expected to rise to 32 per cent by 2050.

Ageing places significant pressure on already highly indebted government finances and will place a heavy tax burden on overstretched younger generations. Favourable regulation can be expected for businesses that assist governments to fund rising healthcare costs.

The intergenerational wealth transfer from baby boomers to their heirs may be the largest wealth transfer in history. This provides valuable opportunities for financial services and consumer goods suppliers. Accenture Consulting expects US$30 trillion to be transferred between generations in the next 30 to 40 years in North America alone.

Mobile data addiction

Growing business and consumer data use especially on mobile devices will boost demand for bandwidth and mobile subscriptions.

Wireless traffic should continue to grow through increased penetration and use of smartphone and tablets to perform a wider range of functions including voice, text, email, calendar management, gaming, music, internet access and an expanding array of other applications.

By the end of 2015 global mobile penetration was 97 per cent according to International Telecommunications Union. There were more than 7 billion mobile subscriptions, up from 738 million in 2000. Mobile broadband subscriptions reached 47 per cent of the global population, 12 times the 2007 figure.

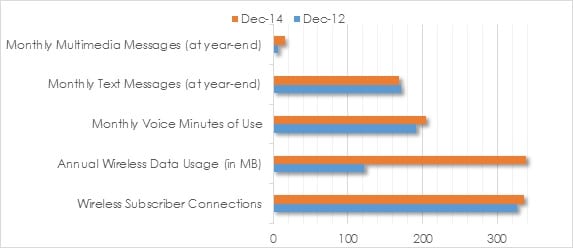

Mobile device users continue to share more information. Indicatively, US monthly wireless data usage grew 66 per cent per annum to 338.4 billion megabytes in the two years to December 2014. Monthly voice minutes grew three per cent per annum and monthly text messaging fell by one per cent per annum, but multimedia messages grew 48 per cent per annum to 15.4 billion.

Wireless subscriptions have grown only one per cent per annum in the period, but smartphones and tablets, which make it easier for users to access and share multimedia content, make up a greater share of devices.

Source: CTIA

Growing investment asset pool

Compulsory superannuation payments ensure a rising investment asset pool driven by Australia’s expanding population and moderately rising wages. This trend provides a significant tailwind for Australia’s financial services providers.

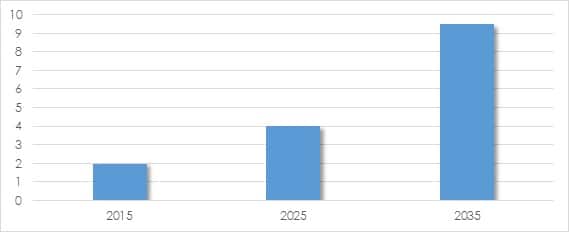

Deloitte expects Australia’s superannuation system to double to $4 trillion by 2025 and reach $9.5 trillion by 2035. Superannuation assets will grow from 120 per cent of GDP currently to more than 200 per cent in 2035. Supporting growth expectations, the Superannuation Guarantee will rise to 12 per cent in July 2025 from 9.5 per cent now. The next scheduled increase is to 10 per cent in 2021.

Source: Deloitte

Andrew Doherty, managing director, AssureInvest