Recently, we looked at the small contribution superannuation is making to Commonwealth tax revenues, making it a target for future measures.

Data just out from the ATO adds a lot more colour to that picture, with detailed statistics released relating to individuals, companies, trusts and, of course, super.

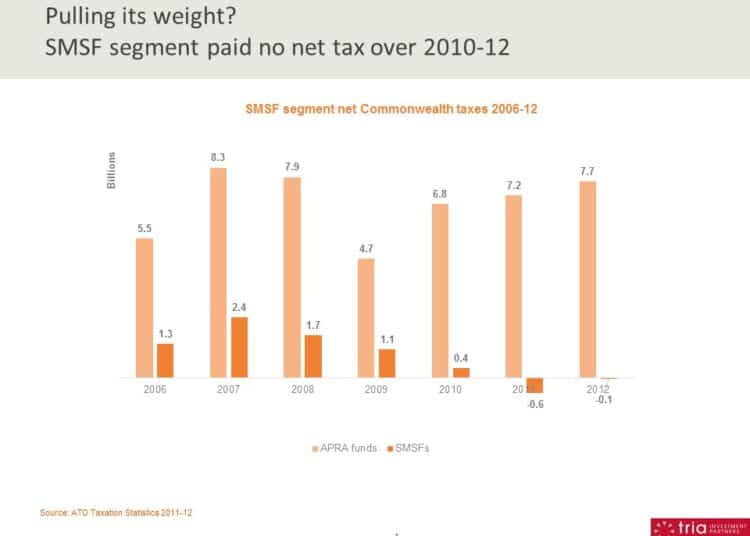

Now we can tell that one of the reasons super is contributing so little to tax revenue is that it appears that SMSFs are paying no net tax – even taking taxable contributions into account – at least for the three years through to 2012.

The chart shows the net tax collected from APRA-regulated funds and SMSFs over the past seven years – covering a cycle of boom, bust, and recovery.

The shape (if not the quantum) of APRA fund tax collections is pretty much what you would expect – rising into the top of the boom, falling sharply in the wake of the financial crisis, and steadily recovering since.

But it’s a different story for SMSFs. Tax collections from SMSFs also rose into the financial crisis and fell afterwards, but unlike APRA funds, they have not recovered. Instead, they have collapsed – indeed the SMSF segment received a net tax refund in 2011 and 2012.

Even at its peak, SMSFs made a much smaller tax contribution per dollar of assets under management than APRA funds. Take 2007: SMSF assets were ~40 per cent of APRA fund assets at that time, but paid only ~30 per cent of the taxes paid by APRA funds.

Jump forward to 2012. The SMSF segment as a whole appears to have paid zero net tax. How was it done?

– SMSFs had gross taxable income in 2012 (including taxable contributions) of $33 billlion

– Take away the $15 billion of taxable income that related to SMSF pension accounts – this is tax exempt. This also indicates that ~45 per cent of SMSF assets are in pension phase (more if the average return on pension accounts is lower than accumulation accounts)

– Fees, expenses, and other deductions came to $3 billion

– This left SMSFs with net taxable income of $15.6 billion – on which indicative tax at 15 per cent would have been ~$2.4 billion. Indeed, the ATO collected $1.2 billion in PAYG installments over the course of 2012

– Yet when the SMSF tax returns as a whole came in, not only did the ATO collect no more net tax beyond the PAYG instalments, it refunded more than the entire $1.2 billion it had collected during the year

– Enter the miracle of franking credits. SMSFs picked up just under $2.5 billion in franking credits over 2012, completely eliminating the segment’s tax bill, and in fact leaving a bit left over

A few points need to be made here.

– This is an overall segment view. Plenty of SMSFs will be paying tax alongside the many that are not

– There will probably be some recovery of SMSF segment tax revenues as investment markets experience positive returns (although there are still a lot of unrealised losses to soak up)

– The issue illustrates last week’s point – that the evolution of the super system towards the pension phase results in substantial erosion of tax revenues. It has already gone a long way in the SMSF segment

That SMSFs have been paying no net tax as a segment does not necessarily indicate tax avoidance, although it will do nothing to quell the concerns of Treasury and others about some of the motivations in the segment. The data supports anecdotal evidence that a commonly marketed benefit of SMSFs is their ability to eliminate tax.

But regardless of the legalities, in an environment where government is looking for more tax revenue contribution from everyone, to have a super segment of one million of the highest account balance members collectively paying little or no tax is simply not a good look. Especially when mum and dad members in APRA funds are still making a significant contribution. It’s hard to imagine that disparity being allowed to continue for long.

Andrew Baker is managing partner at Tria Investment Partners.

James makes an interesting point. The reason Treasury claims (falsely) Australia’s tax to GDP ratio is low compared to European OECD countries is that it ignores this point. Super guarantee levy, workers comp do in Australia what social security taxes do in Europe.

But super here would be doing that job of replacing the age pension better if it were required to be paid as life annuities and there was a $1 for $1 income test against age pensions.

I Hope Mr Bakers ears are burning. He obviously didn’t do much thinking before writing down his wrong headed thoughts. THE REASON GOVERNMENT MADE IT EASY FOR SMSF’s IS BECAUSE SMSF’s ARE DOING THE JOB TRADITIONLY DONE BY GOVERNMENT

The 2 articles that I have seen from Andrew Baker have suggested to me that he is anti SMSFs. Nor does he think clearly when he makes his assertions

Firstly, all superfunds (excluding those in full pension mode)pay tax.

The only reason a superfund gets a tax refund while it supports a TTR pension or is accumulation mode is if the 30% franking credits reduce the tax payable. The tax rate is 15%.

So the effect is that the tax for an accumulation fund is 15% but the franking credits reduce that to zero and the excess of the frankings credits creates a refund.

If a person who had a low taxable income it is possible that that person would receive a full 30% refund. That is 100% more than a superfund.

By extension would Mr Baker suggest that all low income earners or people who do not earn a salary are cheating the taxman if they received a full refund of franking credits?

Apra funds have all the same tax benefits of SMSFs.

Dear Ralph

Investing in an overseas entity does not mean that entity cannot invest back one way or another in Australia. That is what economists refer to as the round-tripping of financial capital. A lot of it is driven by sovereign risk fears: eg Latin Americans putting money in Miami and borrowing it back for local businesses. The point I am making is that silly sovereign risk policies by a Federal Government can produce similar responses. Certainly, it is not easy to navigate all the tax and legal issues but we are talking here about large SMSFs run by sophisticated wealthy families. Non-SMSF investment vehicles are available to them, both onshore and offshore if they wish, and they can invest locally or globally. In fact, anyone with one or two million or more to invest can probably find a suitable vehicle these days.

[quote name=”Dr Terry Dwyer”]One point governments forget. If they attack super funds billions will be heading offshore. There are legal alternative investments in other countries. If they attack a valuable pool of domestic investors who nursed Australian companies through the GFC they will simply expose Australia to more stress next time. But … You can’t tell them.[/quote]

I doubt that a lot of money will move off shore. Most SMSF trustees will only invest locally or have a very small exposure. If they did invest offshore they will lose the benefit of franking credits which account for a lot of the net “no tax payable” situation. Given that Australian shares are some of the highest yielding with refundable credits, why would you swap into a zero tax credit share and risk currency exchange losses as well?

Very simply, the rules are the same for all members of all superannuation funds. Certain individuals choose SMSFs because they are most likely older (and in pension phase) and possibly more capable than the fund managers of looking after their retirement savings. With the proposed fall in the company tax rate all SMSFs will receive a lesser benefit of future franking credits (a substantial government saving I suspect)but I haven’t seen reported yet. Those Funds in pension phase will have a 2% (roughly) reduction in franking credit refunds. I wonder how much the accumulated franking credit balances of ASX listed companies restated from 30% to 28.50% works out to be?

It is obvious Mr Baker has a vested interest in twisting the facts to suit his message. He obviously has not looked beyond his own biased opinion. Mr Baker’s proposals would reduce my capacity to fund my own retirement and possible longevity.

More anti SMSF propaganda from Mr Baker that I see has been picked up again in today’s press. This is a broader super issue so why attack SMSFs? Again a case of any media is good media except ultimately it means zero credibility. Assume Mr Baker is being paid by the big end of town so this line of attack makes perfect sense when outflows to SMSF are the number one issue.

One point governments forget. If they attack super funds billions will be heading offshore. There are legal alternative investments in other countries. If they attack a valuable pool of domestic investors who nursed Australian companies through the GFC they will simply expose Australia to more stress next time. But … You can’t tell them.

APRA and SMSF both operate under the same tax rules – so nothing is happening in one segment that cannot happen in the other. This chart just goes to show why so many people want to operate their own SMSF. Because the APRA funds are full of accumulators while SMSfs have more pensioners. In the APRA funds that I have seen clients in they do not appear to be receiving the full tax beneifts that are going through the APRA funds so opt for a fund that they can manage and benefit from the full tax advantages on offer. I have yet to see a study that shows the effects on APRA funds of their income smoothing (known as reserving ) strategies where they take the members current year income and keep it for a bad year to smooth out their returns & hence look better. Where the member that losses that income may never get the advantage of it. This is not as prevelannt in SMSF where the members can use reserving strategies but often dont wanting to get all the income for the year allocated to them

As the very first commenter here said this is no great secret or surprise as SMSF’s are heavily skewed to pension phase as need to have accumulated enough funds to set up and therefore going to be older members than the general population. Why would the author want to whip up a mere and utterly expected demographic attribute into a “scandal”?

Not that surprising really.

The Government made a mistake when it declared that income generated by the fund would be tax free when a pension started. There is no logical reason for doing so and it has led to people putting as much assets into a low tax or tax free environment as possible.

This is a situation that will increase as SMSF’s grow in value.

Superannuation is not a money pot to be raided by incompetent wasteful governments. Just because it’s there doesn’t qualify it to be expropriated by others. It’s not public money. Taxing super is taking from the future to pay for current consumption. There shouldn’t be any tax on super at all and arguably get rid of the tax deductions as well

Any system works on the basis that the legislature sets the rules, the executive implements them and the judiciary keeps a watching brief. The public should comply – no more, no less.

Emotive words such as miracle franking credits are unhelpful at best and misleading at worst. This is what Parliament intended.

Investing to maximise franking credits, moving into pension phase if done within the rules is what the ATO is expected to enforce. No point whining about it.

As for getting older, I would like to get back into my twenties again, but anyone with a spare time machine?

Let us leave sensationalism and theatrics to the tabloids and movie-makers, people.

Facts will suffice here. Not mangled obfuscation!

The economic value of SMSFs is much broader than how much tax they pay. SMSFs invest half a trillion in the economy, virtually all of it in Australia. The one million Australians who own SMSFs are not a burden on taxpayers when they retire – indeed they are among the 20% of Australians who pay more in tax than they receive in benefits. A dollar invested by the Government in tax concessions is repaid in multiples in age pension savings over a working life. Debate about the appropriate taxation of super savings should take account of their overall benefit to the nation. Hopefully this will be the approach taken in the Tax White Paper flagged by the Government.

SMSF Owners’ Alliance

Andrew Baker, an informative article. Are you working for Bill Shorten?

Dr Terry, good points.

One simple question for Andrew – why are APRA funds so tax inefficient compared to SMSFs?

There’ll be lots of reasons but perhaps, in general, it has something to do with asset turnover through speculation.

SMSFs didn’t create the tax system.

This begs the question – are APRA fund trustees taking their fiduciary responsibilities seriously by not trying to minimise tax payments for their beneficiaries?

Really? This seems Treasury propaganda.

Contributions should be tax-free and earnings should be zero tax, whether in or out of pension mode. That is the logical and correct result of an income tax system which recognized lifetime income averaging.

Otherwise, you punish funded super schemes versus public sector unfunded private ones.

What is more debateable is whether pensions should be tax-free, but that arose out of Treasury’s greed is pre-taxing funds in accumulation mode. It had to give a 15% rebate and most people paid no tax as a result. Further, there is the point that the optimal rate of tax on capital (non-land) income is zero. Having a domestic tax haven supports domestic investment.

What should be accepted is that –

1. superannuation should be drawn as lifetime income (and may be stopped and re-started as needed); and

2. there should be a $1 for $1 income test against all social security benefits.

There are many potential reasons:

1. Contribution caps have significantly reduced and SMSF’s are affected far more significantly than larger funds;

2. Many funds are still carrying capital losses forward, so any gains made are not taxable;

3. SMSF’s are more likely to be holders of shares rather than traders. Most of the larger funds are the reverse and hence, gains are unrealised and hence not taxable.

4. Many pension funds have a portfolio of dividend producing shares or trusts that pass through franking credits. They tend to be net refunds.

5. Hence, funds in accum. mode have lower incomes because they cannot make tax deductible contributions any near as high as they used to a few years ago, are not reporting capital gains and their share portfolios have recorded pretty good yields over the last few years. Hence, no surprise, tax take is down because of Govt actions and market actions. No conspiracy, totally predictable.

I have no doubtif Treaury looks at these statistics they will re-visit increasing tax rates in earnings in pensions over $100K.

My guess is that most APRA funds are in accumulation mode, whereas a large number (45% according to the writer) of SMSF are in pension mode. Many entities use franking credits to reduce their tax – all legal and above board.

Yes, there is not a lot of tax paid the the sector, but the sector is not putting their hand in the public purse (pensions etc). Most of the SMSF pensioners do not get/ask for any benefits from the state – just want to be left alone and get on with life.

Stop knocking the sector and conce=ntrate on getting better returns for your members – that is why SMSF exist!