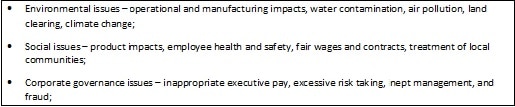

Investment performance isn’t just driven by what is reported in financial reports or incorporated in analyst estimates. Companies that ignore the environmental, social and governance (ESG) impacts of their business leave themselves open to financial losses, brand damage, litigation and shareholder activism – ultimately risking their social license to operate.

As explored by MSCI (Morgan Stanley Capital International) in the research paper “Can ESG add Alpha?”, investing in a portfolio of global companies which have higher ESG ratings than their peers was found to outperform the benchmark by 1.1 per cent per annum with less volatility, thus giving investors a superior absolute return over the period of February 2007 to February 2015.

Investing in a portfolio of companies that are improving their ESG track records was also found to outperform, in this instance by 2.2 per cent per annum. Improvements help to re-rate the stock, reducing “potential future liabilities” that may be incurred while demonstrating that the companies are “equipped to avoid ESG-related risks”.

Investing responsibly is part of a trustee’s fiduciary duty, so taking into account the ESG risks that an investment is exposed to makes good financial sense. SMSF investors should be looking to incorporate ESG risk analysis into their investment process because, in essence, investing with an ESG lens is a proxy for quality. It’s an indicator that a company is stable, efficient and well managed, and marks those who are focused on sustainable long-term growth.

Taking a responsible investment approach is also a way to provide SMSF investors with the peace of mind that their super is being invested in the future that they want to retire in. SMSF investors with their own equity (and bond) portfolios are in a unique position to exclude companies involved in activities that they deem unethical. They can also proactively invest in companies mitigating the risks of, and transitioning to adapt to climate change.

Those investing in funds can now access a growing range of responsibly invested and ESG integrated strategies in all asset classes, offered by over 70 managers. The Responsible Investment Association Australasia (RIAA) reported in their “Responsible Investment Benchmark Report 2016” that the average performance of responsible Australian share investment strategies which screen, or invest with a sustainability or impact theme, outperformed core peers and the S&P/ASX300 over one, three, five and 10 year periods. In global equities, the average performance of responsible investment strategies ranged within ±3 per cent of the MSCI World ex Australia over the same time periods, with some managers reporting stellar outperformance and others strong underperformance.

The importance of investment selection should not be underestimated and SMSF investors taking a responsible investment approach can potentially gain from the benefits of ESG risk management: lower volatility and thus higher long-term performance. Their ability to invest with the values they believe is their free-lunch to a good night’s sleep.

Jodie Tapscott, senior manager, corporate responsibility, Colonial First State

{kind=link}

So if a fund manager invests in ESG companies because of their own personal and political leanings, rather than for the benefit of the client, and those investments crash and burn does that leave them open to action? Something about fiduciary duty comes to mind……

Neither you nor Terry seem to have read the article which clearly states that there is strong evidence of these issues impacting risk and return and so directly part of relevant trustee considerations. Don’t take my word for it:

Noel Huntley SC opinion

https://cpd.org.au/2016/10/directorsduties/

UNPRI assessment of 8 markets including Australia

http://www.unepfi.org/fileadmin/documents/fiduciary_duty_21st_century.pdf

APRA climate change speech

http://www.apra.gov.au/Speeches/Pages/Australias-new-horizon.aspx

The evidence of strong links between ESG issues and long-term performance is also extensive as shown by the DB in this meta study, the most comprehensive performed to date:

https://www.db.com/newsroom_news/2016/ghp/esg-and-financial-performance-aggregated-evidence-from-more-than-200-empirical-studies-en-11363.htm

But your first step should be to actually read what has been said!

This sounds like useless bureaucratic/management-speak. If a company is acting within the law and making good profits and paying good dividends trustees are free to buy into it. The Scargill case in the UK makes it perfectly clear it is improper for trustees to invest for any other purpose than maximizing returns long term. Certainly, if you see in 2017 the coal trade may be abolished in 5 years, you may choose to exit but opinions will vary. In fact, as silly groupthink corporates exit some large industries for fear of noisy protests, the assets they are selling may become more attractive to SMSFs.

That said, personally I am not interested in investing in brothels, arms dealers and tobacco and that is my prerogative as an SMSF beneficiary but not mine as a trustee. Big corporate trustees don’t seem to understand the difference and are seeking to impose noisy trendy views on their hapless clients.

Terry Dwyer

Dwyer Lawyers

Hi Terry Please see the reply to Wayne below which also relates to your comments

.

Also the Scagill case is frequently misunderstood and Scargill himself has said so. For a more accurate reflection on this and the broader body of UK law well worth checking out the UK Law Commission review: http://www.lawcom.gov.uk/wp-content/uploads/2015/03/lc350_fiduciary_duties.pdf

There really is no excuse for improperly relying on Scargill anymore, the record has been well and truly (and repeatedly) corrected.

To do what this person suggest may breach the sole purpose test. Moneys in a smsf are for the benefit of the members not the environment. So unless the returns justify it i would not include social responsible inveating in an smsf investment strategy